Did you know? General Partners (GPs) notices are among the most frequent yet undervalued communications in private market funds. For Limited Partners (LPs), managing these notices effectively is critical to maintaining compliance, optimising portfolio decisions, and strengthening GP relationships.

In this guide, we’ll break down the essentials of GP notices - from their structure and purpose to how you can overcome common challenges. Whether you’re part of the investments, operations, or accounting team, this blog will equip you with the insights you need to streamline your processes and make data-driven decisions.

How GP Notices Work

How GP Notices Work

One of the distinctive features of private market funds is the way capital moves in and out of the fund. LPs commit capital upfront, but GPs draw down this capital gradually over several years, depending on the pace of investments. Likewise, GPs return capital to LPs in multiple instalments as they liquidate investments. In essence, GPs call capital and distribute proceeds as needed, rather than following a fixed schedule.

Notices are the formal document through which GPs communicate to LPs when and how much capital needs to be contributed or distributed, and generally fall into two main categories: call notices and distribution notices.

Call notices

Through call notices, General Partners (GPs) request Limited Partners (LPs) to contribute capital for purposes such as:

- Making new investments

- Supporting existing investments

- Covering management fees and fund expenses

Most calls occur during the first five years of a fund’s life, known as the “investment period,” to finance new investments. However, calls may still be issued during the second half of a fund’s life to fund follow-on investments. Also, at any point in the fund's life, calls are made to cover management fees and expenses.

Capital calls typically reduce the unfunded commitment. For example, if your unfunded commitment is $1,000,000 and you receive a call for $200,000, the updated unfunded commitment is generally reduced to $800,000. An exception to this occurs with calls classified as “out of commitment.” In general, the notice will usually specify the impact on the unfunded commitment and highlight whether the call should be treated as "in" or "out" of commitment.

Distribution notices

Via distribution notices, GPs instead notify LPs of payments directed to them. These may due to:

- Income generated by existing investments

- Proceeds from partial or total exits

For example, imagine a GP successfully exits an investment, generating proceeds. You receive a distribution notice stating you will receive $150,000 as your pro-rata share of proceeds: $100,000 as return of capital, and $50,000 as realized gain. This distribution reduces your invested capital by $100,000, returning a portion of your original commitment, while the $50,000 realized gain represents profit earned from the investment.

For buyout and venture capital funds, distributions usually start only in the second half of a fund’s life (the “harvesting phase”) as the bulk of distributions comes from the sale of portfolio companies. For income-generating strategies such as Private Debt, you can expect to receive distribution notices from year 1.

Distributions generally do not impact unfunded commitments. However, if a distribution is classified as "recallable" under the fund's limited partnership agreement (LPA), it increases the LP's unfunded commitments, effectively raising the amount of money that can be called by the GP in the future.

Simultaneous Calls and Distributions

There are instances where GPs may issue a single notice that combines both call and distribution components. For example, this could happen when proceeds from a company sale are distributed to LPs while simultaneously calling for funds to cover management fees. In such cases, the GP issues a single notice and offsets the call and distribution amounts. The end result can be either a “net call” or “net distribution”, depending on which component outweighs the other.

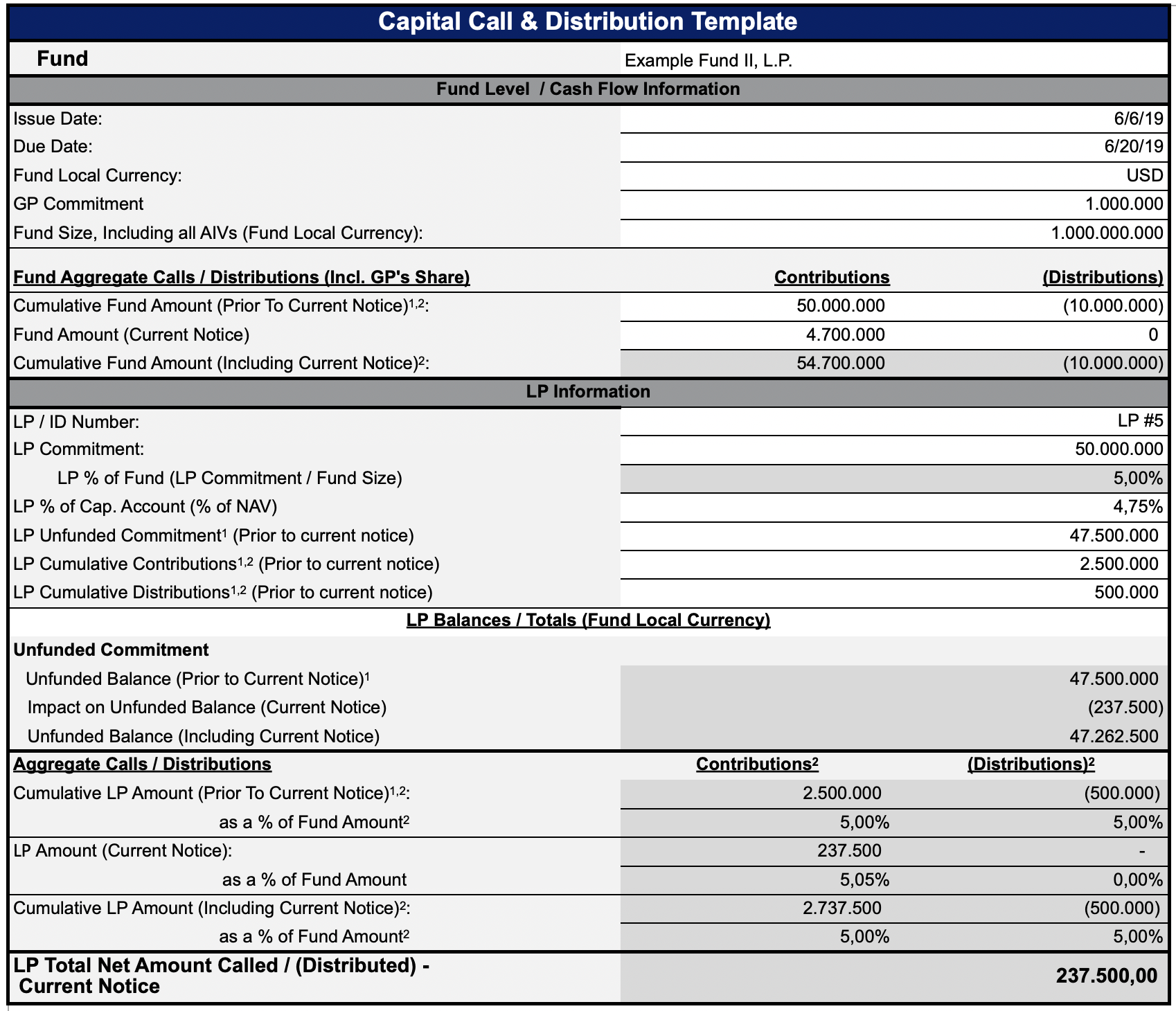

Anatomy of a GP Notice

What information do you actually find in a notice? GP notices contain critical details that LPs need to review carefully. Here are the key elements to look for:

- Fund Details: the name of the fund issuing the notice

- LP Details: name of the specific LP to whom the notice is addressed

- Issue Date: the date on which the notice was issued

- Payable Date: deadline by which payment needs to be wired or will be received

- Net Amount: the total amount either due to or receivable by the LP

- Breakdown of Calls: split between investments, management fees, and expenses; calls may be further classified as in-commitment or out-of-commitment, depending on whether they reduce unfunded commitments

- Breakdown of Distributions: split between income, return of capital, or realised gains; distributions may be further classified as recallable or non-recallable, depending on whether they increment unfunded commitments

- Equalisations: reallocations of previous calls and distributions to account for new LPs joining the fund

- Unfunded Commitment: the unfunded commitment is typically reduced by in-commitment calls and increased by recallable distributions. It is generally stated explicitly, as edge cases or exceptions are often addressed in the Limited Partnership Agreement (LPA). In some cases, the notice reports the unfunded commitment both before and after the notice.

- Commentary: additional context regarding the notice, such as details about a new investment or the realization of an asset.

- Payment Details: for distributions, includes the necessary bank account information and instructions to process the payment.

Not all notices will include every element listed here, but these are useful details to keep in mind when reviewing one.

Here is an example following the standards set by the Institutional Limited Partners Association (ILPA):

Understanding How LPs Process Notices

Before diving into the specifics of which notice information LPs should prioritise, it’s important to understand how these documents are processed and used by various stakeholders within an LP organisation.

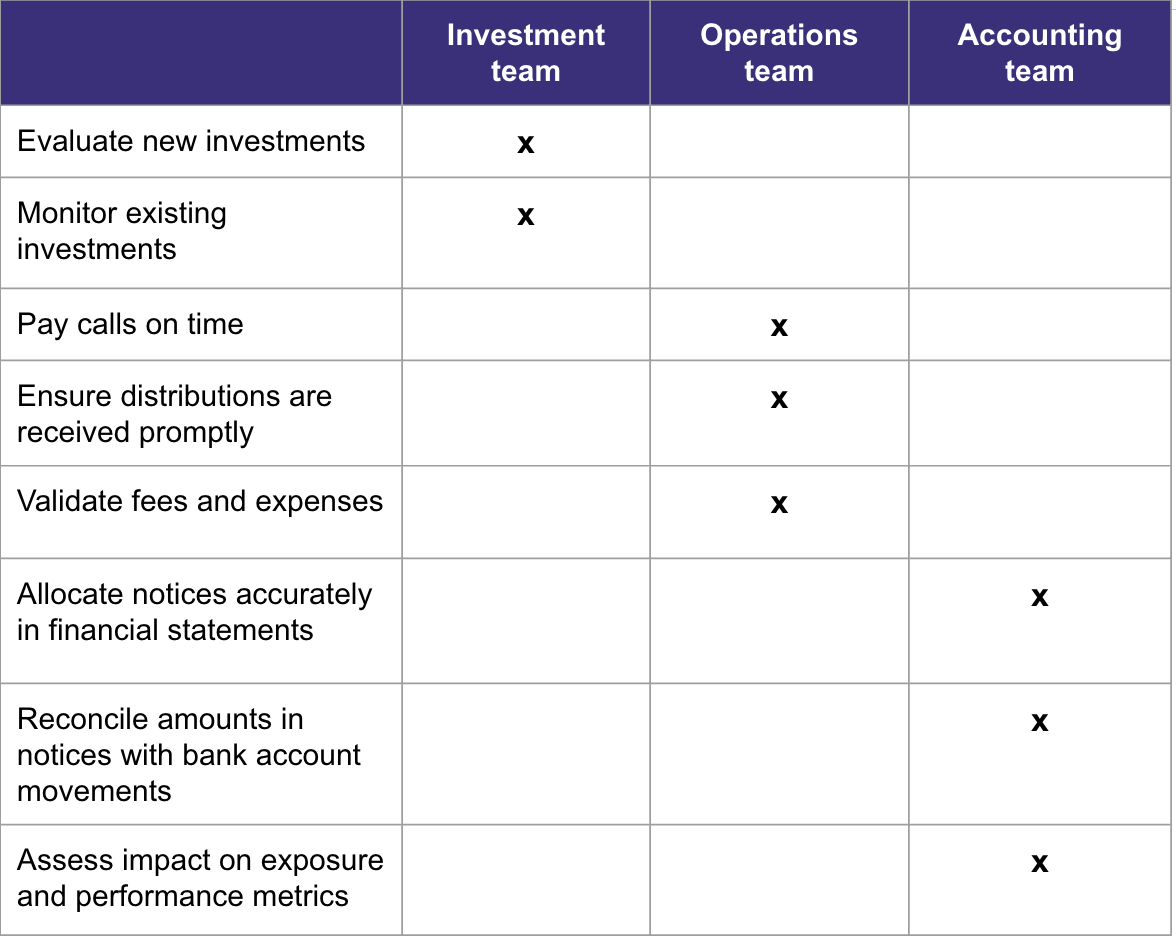

While every LP structure is unique, they typically consist of three key teams with distinct roles:

Investments Team

The main focus of the investment team is to evaluate new investments and monitor existing ones. As a consequence, their primary interest for notices is about the transactions that may cause the call or distribution:

- What new investment has been made?

- What investments have been exited?

- Are these actions aligned with the GP’s investment strategy and guidance?

- How do these transactions impact portfolio exposures and construction?

- What is the effect on overall performance?

Essentially, they treat the notice as a "live signal" of investment activity, helping to confirm or refine their understanding of the GP's strategy. For them, the most valuable part of the notice is the narrative surrounding the transaction and components of calls and distributions.

Operations Team

The operations team is normally responsible with actioning the information contained in the notice:

- Paying calls on time: missing deadlines could result in penalties, interest charges, or strained GP relationships

- Ensuring distributions are received promptly

- Validating fees and expenses against the Limited Partnership Agreement (LPA) and side letters

As a consequence, the team will mostly focus on payable dates, net amounts, and GP bank account details.

Accounting Team

Last but not least, the accounting team is usually tasked with maintaining an accurate picture of financials. Key tasks include:

- Allocating notices accurately in financial statements

- Reconciling amounts stated in notices with actual bank account movements

- Assessing the impact on exposure and performance metrics

To this end, the team will be particularly attentive to the breakdown of calls and distributions into individual components, and to the impact on unfunded commitments and overall financial metrics.

By understanding how each team utilizes GP notices, LPs can better streamline processes and ensure that all relevant data is extracted.

Here is a summary of which fields are likely to be used by LP stakeholders:

What Information Should You Collect?

To meet your organisation’s needs effectively, it is essential to define a clear strategy for data collection. This involves addressing three key questions:

- Identify Required Fields: determine which fields need to be collected consistently, based on your specific use cases (as discussed in the previous section)

- Hande Missing Information: define a process for managing incomplete data and addressing gaps to maintain accuracy. For instance - if you receive a call without any split out, should you treat it as called for investments?

- Standardise Data Classification: develop a framework for reclassifying data to ensure consistency across all records. For instance, if the GP withholds management fees from a distribution, should you reclassify that item as a call for management fees, rather than treating it as a (negative) distribution?

How Tamarix Can Help

Managing General Partner (GP) notices can be overwhelming, especially for Limited Partners (LPs) with investments across multiple funds. Extracting, categorising, and tracking notice data demands significant time and resources. Tamarix addresses these challenges by offering AI-driven solutions that save 100s of hours each month:

- Notices Tracking: Tamarix employs advanced AI to extract key information from GP notices, regardless of format.

- Normalisation and Categorisation: our platform standardises data across funds, facilitating easier analysis and comparison.

- Data Storage and Analytics: we provide secure data storage coupled with powerful analytics tools, enabling deeper insights into fund investments.

By leveraging Tamarix, LPs can streamline workflows, reduce manual errors, and gain a comprehensive understanding of their investment portfolios.

Conclusion

GP notices play a crucial role in LP fund management, serving as a key communication channel between GPs and investors. By understanding the purpose of these notices, familiarising yourself with their structure, and addressing common challenges, you can streamline notice management and make more informed investment decisions.

Ready to take control of your GP notices?